2026-05-13

Accountancy is a crucial business function for organisations, providing accurate financial data for decision-making, compliance and performance analysis. While many view accountancy as one discipline, it can actually be broken down into several specialised branches within an organisation, each addressing a different function.

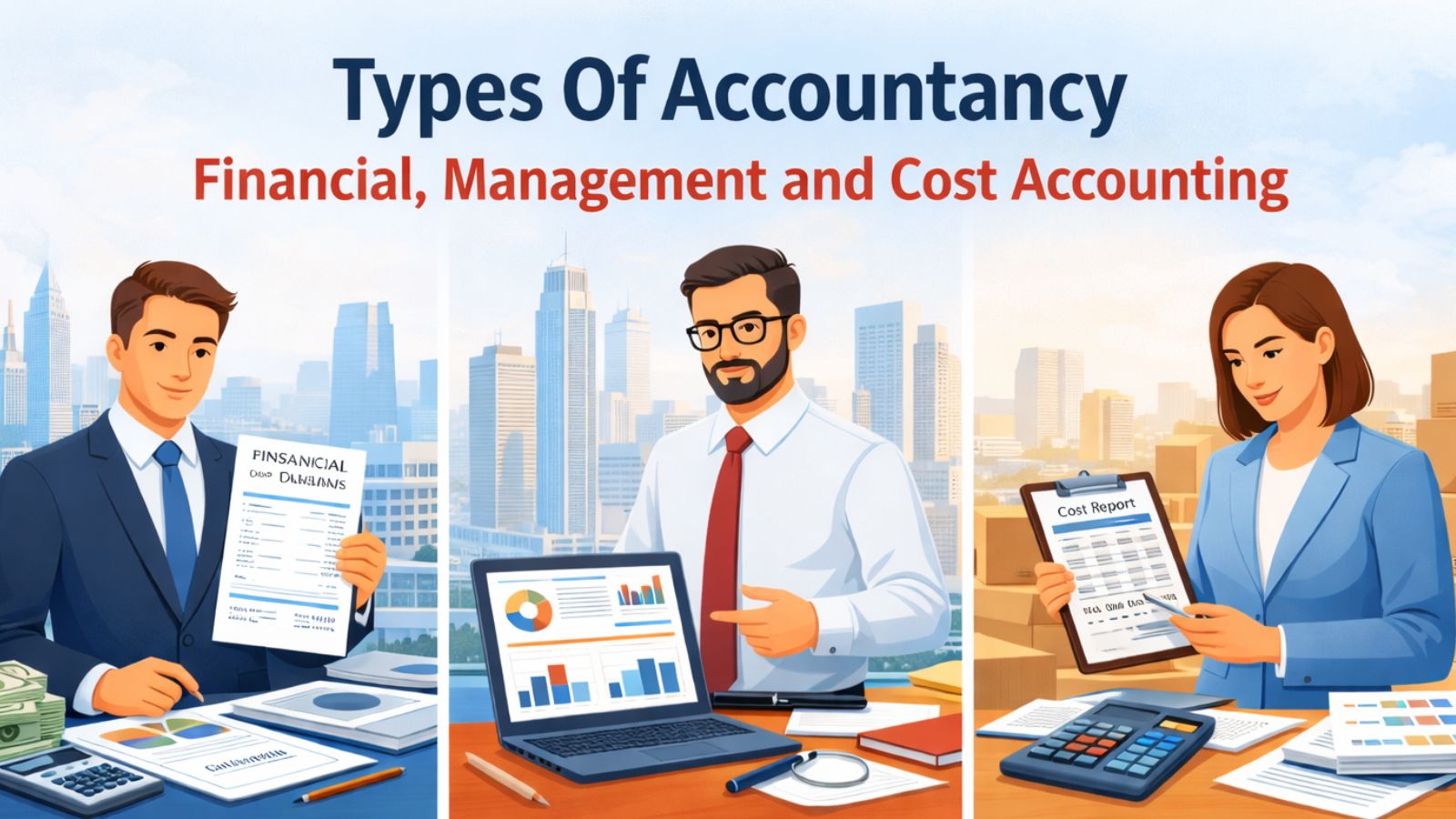

Three main types of accountancy are Financial, Management and Cost Accounting. Understanding the differences between these branches of accountancy will help students, businesses, and professionals determine which approach or career path best aligns with the needs of their organisation.

The main purpose of financial accounting services in UAE is to ensure that all transactions that take place within an organisation are recorded, summarised and properly presented for a specific period of time. The ultimate goal of accounting is to develop financial statements that can be used for various purposes to represent the financial position and performance of the organisation.

The outcome of financial accounting will be the following outputs: income statement (profit and loss account), balance sheet, cash flow statement and statement of changes in equity (changes in owners’ equity). The three statements give an overview of the performance of an organisation with respect to profitability, assets, liabilities and cash flow.

There will be a large volume of financial accounting data available for use by external stakeholders. External stakeholders are generally defined as those parties that will use the data produced by an organisation. External stakeholders may include:

(i) investors and shareholders

(ii) creditors and lenders

(iii) tax authorities

(iv) regulators.

The key characteristics of financial accounting are:

(i) there are standardised accounting principles

(ii) the information produced by accounting is based on the historical record of activities that occurred prior to the reporting date

(iii) that security laws and regulations require public companies to use accounting

(iv) that the intent of financial accounting is to produce an accurate and transparent (consistent) report on the financial performance of a company.

One of the primary purposes of financial accounting services in UAE is to align with the law. Another objective is to foster investor confidence. Finally, both investors and creditors use financial accounting to evaluate the financial position and viability of a business.

Management accounting (also known as managerial accounting) is a form of accounting that provides management with both financial and non-financial information to facilitate planning, controlling, and making business decisions internally. Management accounting differs from financial accounting in that it looks forward (future) rather than backward (historical). Consequently, management accounting can help organizations operate more efficiently and perform strategically better.

Management accounting provides important functions to management, including:

The primary users of management accounting are (internal) stakeholders, including:

Management accounting does not adhere to strict rules regarding standardization. Management accounting is designed to provide a future-oriented analysis of management decisions. Management accounting will be tailored to meet the specific needs of each organization and will include both financial and operational data.

Management accounting helps organizations make informed strategic decisions, allocate resources efficiently, and maintain competitive advantage in dynamic business environments.

Cost accounting focuses on determining, analyzing, and controlling the costs associated with production or service delivery. It plays a crucial role in cost management and pricing decisions.

Cost accounting is particularly important in manufacturing, logistics, and service-based industries where cost efficiency directly impacts profitability.

Cost accounting involves:

Cost accounting information is used primarily by:

By controlling costs and improving efficiency, cost accounting helps organizations maximize profits without compromising quality or productivity.

All three forms of accounting (Financial, Management and Cost) rely on information provided by the others for their respective functions. Cost Accounting data feeds into Management Accounting to assist with analysis and decision making; whereas Financial Accounting utilises summary data from the other two forms to generate statutory financial statements. All three provide the overall view of how an organisation is performing and how solvent it is financially.

Knowledge of Financial Accounting, Management Accounting and Cost Accounting is fundamental to the effective management of any organisation and to the professional development of a business manager. Each has a specific role; however, combined they enable better financial management, strategic planning and ultimately the long-term success of an organisation.

If you are a student considering your career options, a business owner maintaining your financial records or a professional who is looking to specialise in one or more of these areas, knowledge of these three areas of accountancy will provide you with a solid basis for making informed decisions.

The three main types of accountancy are Financial Accounting, Management Accounting, and Cost Accounting. Each serves a different purpose within an organisation—financial reporting, internal decision-making, and cost control, respectively.

The primary objective of financial accounting is to record, summarise, and present an organisation’s financial transactions accurately for a specific period, resulting in statutory financial statements that reflect the company’s financial position and performance.

Financial accounting information is mainly used by external stakeholders, including investors, shareholders, creditors, lenders, tax authorities, and regulatory bodies.

Management accounting focuses on future-oriented planning and decision-making, providing both financial and non-financial data for internal management. In contrast, financial accounting is historical and compliance-driven, primarily serving external stakeholders.

Cost accounting helps organisations analyse, control, and reduce costs related to production or service delivery. It supports pricing decisions, profitability analysis, and operational efficiency, especially in manufacturing and service-based industries.

Cost accounting provides detailed cost data that supports management accounting for planning and decision-making, while financial accounting uses summarised information from both to prepare statutory financial statements. Together, they offer a complete view of an organisation’s financial performance and stability.

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test