2026-05-12

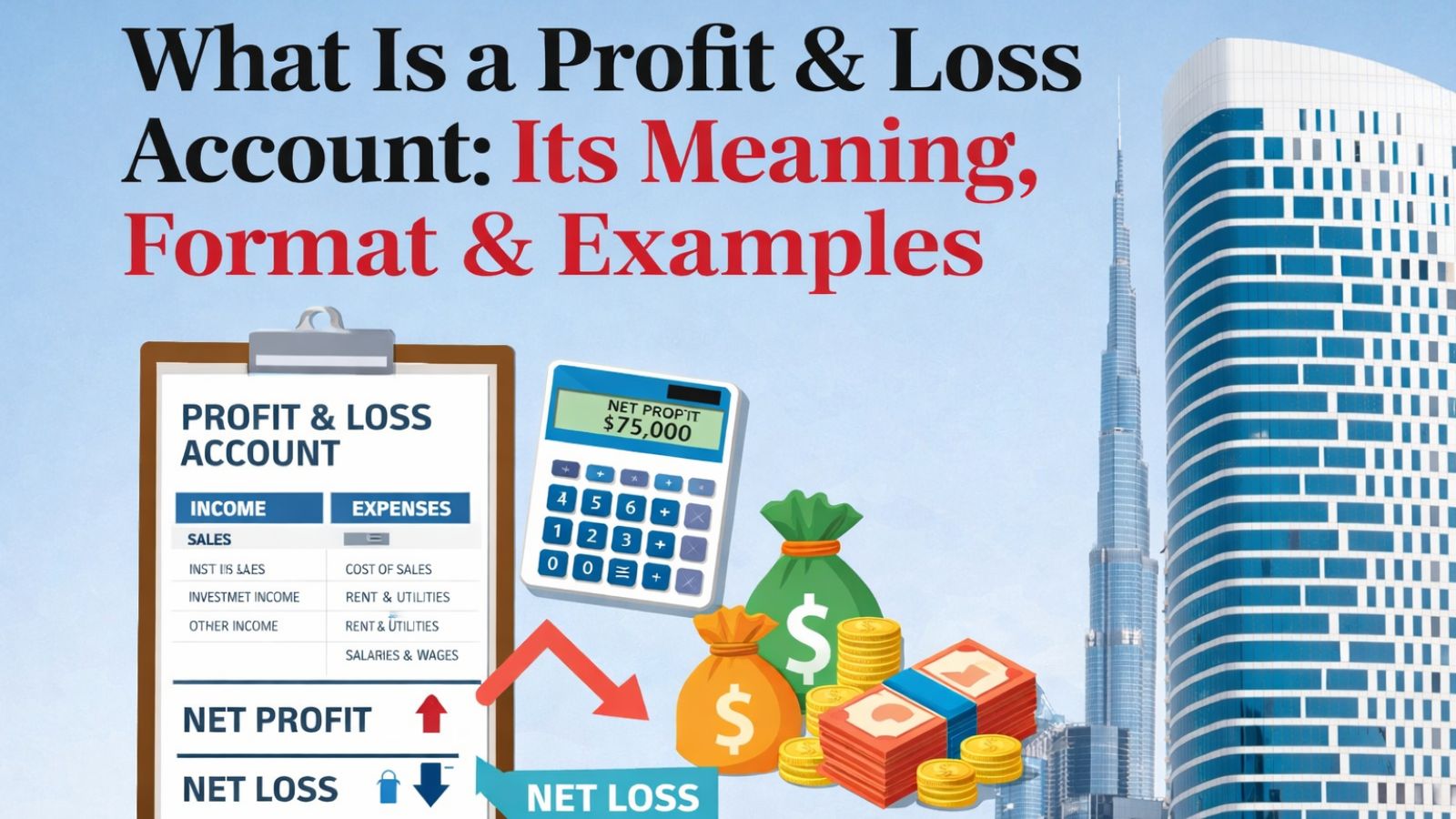

Profit & Loss Account (P&L account) is one of the most informative financial statements used by businesses. It provides an indication of whether the business has made a profit or experienced a loss during the stated period (for example, the past year). Due to its role in assessing the economic performance and operations of the business, the Profit & Loss Account is used by both business owners and managers, as well as potential investors and lenders.

We will define a Profit & Loss Account, describe how it will be formatted, the functions of a Profit & Loss Account, and provide real-life examples of how to use it.

The Profit & Loss Account is frequently called an Income Statement or Statement of Profit and Loss. It summarizes the revenue earned, the expenses incurred, and the costs associated with running the business during a specified period (typically monthly, quarterly or annually).

Main objectives of a Profit & Loss Account is to:

Example of this would be the following equation:

If the total amount of income is greater than the total amount of expenses, the company has earned a profit. If the opposite is true, the company has incurred a loss.

It’s an overview of different types of objectives of a P&L Account.

Measuring the operational performance of a business, identifying profitability trends over time, and helping to manage cost and expense control, assist management to make decisions (pricing strategy, expansion strategy, cost reduction strategy, etc.) and serve as a source of information for investors, lenders, and tax authorities.

In practice, many businesses rely on professional accounting & bookkeeping services in UAE to ensure their Profit & Loss Accounts are prepared accurately, comply with local regulations, and support informed financial decisions.

The basic elements of a Standard P&L Account consist of Revenue/Income, Cost of Goods Sold (COGS), Gross Profit, Operating Expenses, and Operating Profit.

Revenue/Income is the total amount of money that has been made from the business’ core products/services. This would include Sales Revenue, Service Income, and Commissions (or other fees such as agents/finder’s fees).

Cost of Goods Sold (COGS) represents the total of the direct expenses of producing the product or service including Raw Materials, Direct Labor, and Manufacturing Expenses.

Gross Profit = Revenue – COGS, and represents how effectively the business produces/Sells; therefore it is the measure of how efficient the business is.

Operating Expenses are the total of indirect expenses required to operate the business, including Rent, Salaries & Wages, Marketing & Advertising, Utilities, Office Expenses, and Depreciation.

Operating Profit = Gross Profit – Operating Expenses. Operating Profit is the business’ income minus the business’ non-income expenses, and is therefore the profit from core business operations prior to Interest and Taxes.

These include:

This is the final result after all incomes and expenses:

Net Profit/Loss = Total Income – Total Expenses

The P&L account can be prepared in two commonly used formats:

| Expenses (Debit Side) | Amount | Income (Credit Side) | Amount |

| Cost of Goods Sold | XXX | Sales Revenue | XXX |

| Salaries | XXX | Other Income | XXX |

| Rent | XXX | ||

| Utilities | XXX | ||

| Net Profit | XXX | ||

| Total | XXX | Total | XXX |

Revenue

The statement format is more widely used today, especially in corporate financial reporting.

Let us consider a simple example of a small business for one financial year.

Revenue

Less: Cost of Goods Sold

COGS = ₹4,50,000

Gross Profit = ₹5,50,000

Operating Expenses

Total Operating Expenses = ₹3,30,000

Operating Profit = ₹2,20,000

Less: Interest Expense = ₹20,000

Net Profit = ₹2,00,000

This means ABC Traders earned a net profit of ₹2,00,000 during the year.

The Profit & Loss Account (P&L) is an important document for both internal and external stakeholders and is used to show the ability of the business model to operate profitably over time, evaluate performance against historical benchmarks and calculate and report required tax obligations. The information within a P&L Account allows investors the opportunity to evaluate both profitability and risk, which is critical for making investment decisions, and also assists with the development of budgets and long-term strategies.

The P&L Account is an overview of the financial performance of the business and provides a historical perspective on how well the company is doing. As such, understanding the terminology, structure and meaning of a P&L Account is essential for effective financial management, whether you are operating a small business or responsible for managing the finances and evaluating future investment opportunities for a large corporation.

When a P&L Account is prepared properly, it can serve not only as a compliance document but also serve as a strategic tool that can be used to create a solid plan for the future through sustainable growth.

A Profit & Loss Account is a financial statement that shows a business’s income, expenses, and profits or losses over a specific period. It helps determine whether the business has operated profitably during that time.

The main purpose of a Profit & Loss Account is to measure the financial performance of a business by comparing total income with total expenses, enabling stakeholders to assess profitability and operational efficiency.

The key components include revenue or income, cost of goods sold (COGS), gross profit, operating expenses, operating profit, non-operating income or expenses, and net profit or net loss.

Gross profit is calculated by subtracting COGS from revenue, while net profit is the final profit after deducting all operating and non-operating expenses, including interest and other costs.

The two commonly used formats are the traditional T-format and the modern statement format. The statement format is more widely used today due to its clarity and suitability for financial reporting.

A Profit & Loss Account helps business owners and managers track profitability trends, control costs, plan pricing strategies, and make informed decisions related to expansion, budgeting, and long-term growth.

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test