The UAE has brought new VAT Law related administrative penalty changes into force from 14th April 2026 under Cabinet Decision No. 129 of 2025.

For full details and evolution of the VAT Law related administrative penalties, refer to the Table.

In plain terms, this is a shift from a harsher penalty model to a more measured one (aligning them and in line with Corporate Tax related administrative penalties). The direction is clear: the UAE still expects accuracy and timely compliance, but it is now giving more room for correction, voluntary disclosure, and regularisation of records before matters become expensive. That is the real message behind this change.

For instance, change in tax record updates. If a registrant fails to notify the Authority of an amendment required in its tax record, the new penalty is AED 1,000 per violation, rising to AED 5,000 if the same violation is repeated within 24 months. The official table expressly introduces this 24-month repeat-violation window.

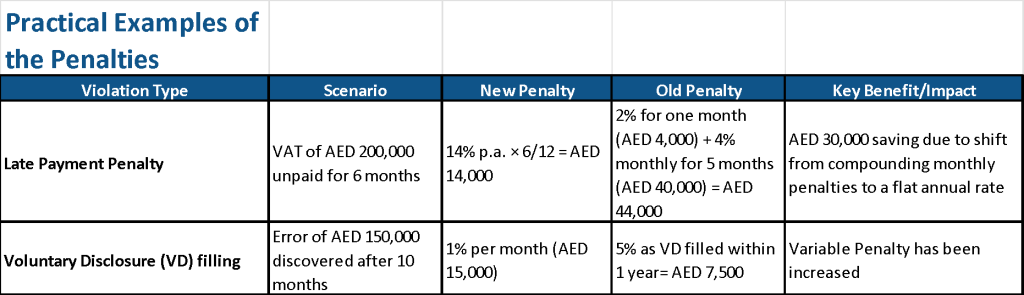

The late payment penalty has also changed materially. The official decision now applies to a monthly penalty of 14% per annum, charged for each month or part thereof on the unpaid tax amount from the day after the due date. This is one of the biggest reductions compared with the earlier system (again, making it in line with Corporate Tax-related administrative penalties)

For an incorrect tax return, the new rule is far lighter in many normal cases. The official penalty is now AED 500, unless the registrant corrects the return within the filing deadline or submits a voluntary disclosure that does not create a tax difference. This is a notable softening from the earlier fixed-penalty approach.

The treatment of voluntary disclosures is also more structured now. Where a taxable person submits a voluntary disclosure for errors in a tax return, tax assessment, or refund application, the official rule imposes a 1% monthly penalty on the tax difference from the day after the original due date until the voluntary disclosure is submitted. Where the person fails to submit a voluntary disclosure before being notified of a tax audit, the decision imposes two penalties: a fixed 15% on the tax difference, plus a 1% monthly penalty on the tax difference for the relevant period.

For more VAT-specific administrative lapses, the framework remains focused on invoicing discipline. The official VAT penalty table continues AED 5,000 for failure to display prices inclusive of tax, and AED 2,500 per detected case for failing to issue a tax invoice, tax credit note, or comply with e-invoicing document procedures where applicable under VAT law.

What should businesses do now? Review old open exposures, late payments, pending corrections, tax record changes, and submit errors immediately. This is the kind of update that rewards clean-up action. The law has become more forgiving, but only for businesses that move quickly and keep their records in order. Waiting carelessly is still a bad strategy.

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test