2026-05-19

Tax compliance has progressed beyond awareness for companies in the UAE. What initially felt like a new regulatory shift in 2023 has now become an active part of running a business in the UAE; with stricter enforcement, tighter filing expectations, and increasing scrutiny from the Federal Tax Authority (FTA).

Even though many companies have mastered corporate tax basics, some are still at risk due to mistakes that slip in every stage of the process; whether it be registration, tax filing, or Free Zone qualification.

Most of the time, the issue itself isn’t intentional, rather a misunderstanding of rules or lack of clarity on deadlines. These can lead to several consequences including penalties, delayed approvals, audit exposure, banking complications, or the loss of preferential tax treatment for your business.

In this guide, we’ll be breaking down five common corporate tax mistakes and their implications on your business.

If you’re making any of these mistakes, it’s important to recognize any risks created by them and strategize on how you can take the next step forward.

Corporate tax compliance must be built gradually throughout the year. This includes accurate bookkeeping, invoicing, expense tracking, and payroll records.

Yet, it’s reduced to a last-minute activity that is given priority only when filing time approaches.

Ideally, by the time a return is due, compliance work should already be complete. Businesses waiting until filing season to sort out accounts often struggle to reconstruct financial records, track undocumented expenses, and rectify inconsistencies.

This approach might seem to save time, but it only creates risks. For instance, deductible expenses may be lost simply because supporting documentation was never properly maintained; or, financial statements may require expensive IFRS adjustments before filing. In some cases, rushed or inaccurate tax returns can provoke unnecessary scrutiny by the FTA.

Companies are now expected to make real-time, accurate record keeping as part of standard compliance, thanks to the mandatory e-Invoicing in 2026,

So, if your business has to get all financial records sorted by January, all compliance work should be done by September to maintain accuracy of your records.

VAT and corporate tax are completely separate regimes. They have separate registrations, Tax Registration Numbers (TRNs), filing schedules, and penalties. From the FTA’s standpoint, both obligations are monitored independently.

So, even if you’re VAT compliant, it doesn’t automatically make your business corporate tax compliant.

Now, some companies may assume that their existing VAT TRN covers corporate tax registration. Even the VAT logic doesn’t apply to corporate tax calculations, since the rules, deductions, and reporting structures work very differently.

The next mistake is when a business relies heavily on VAT returns as a substitute for proper financial reporting. This indicates a false sense of security; A company may appear organized for its up-to-date VAT filings, while still being fully non-compliant from a corporate tax perspective.

Then comes the deadline confusion. VAT and corporate tax follow a different cycle, and confusing the two could lead to missed registration or filing deadlines.

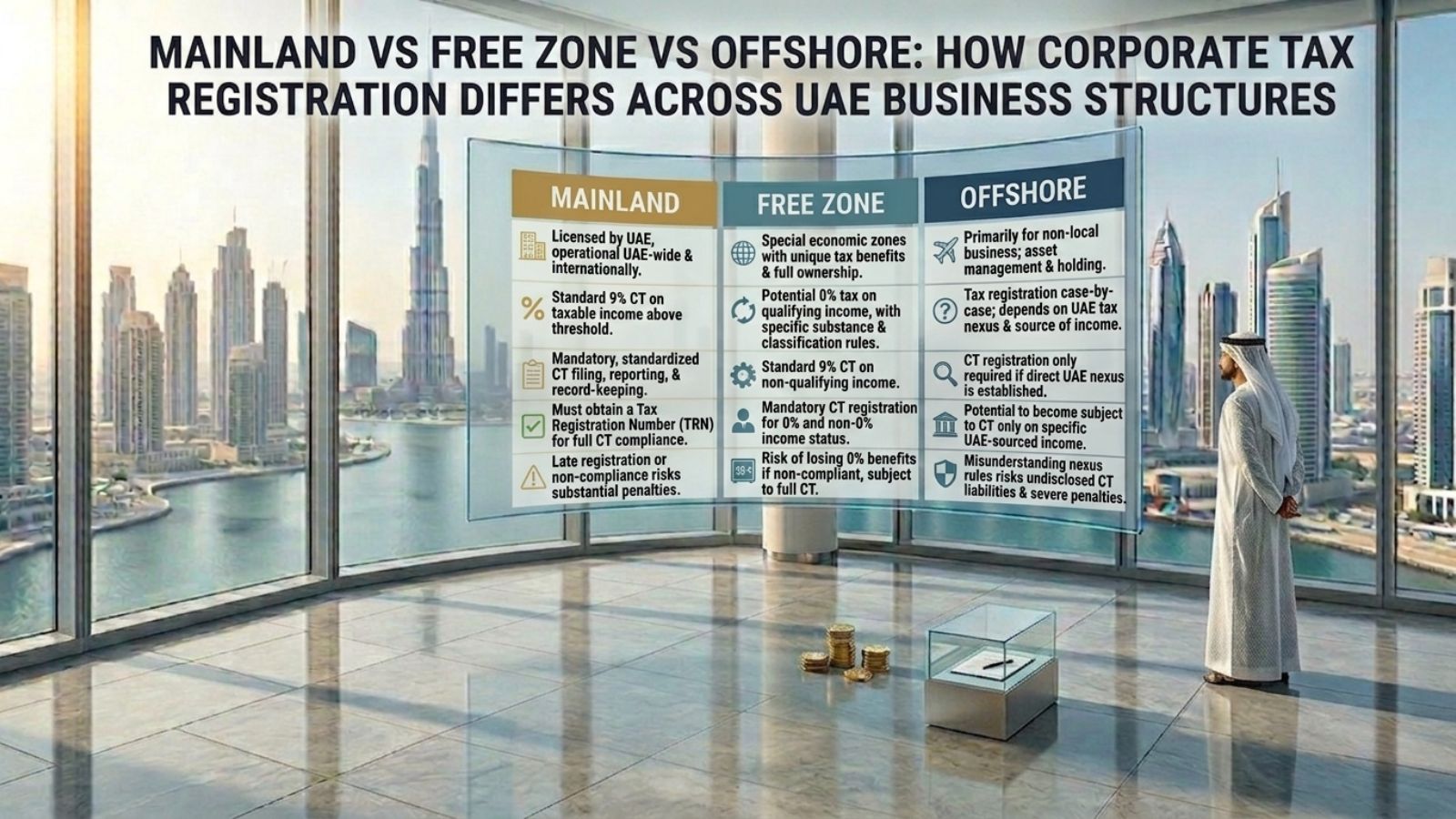

It’s still assumed that the Free Zone business doesn’t have to pay any corporate tax rate. But the truth is, Qualifying Free Zone Person (QFZP) must be actively maintained and reassessed every year. It’s neither automatic nor permanent.

This is where exposure to tax risk can start. If a free zone business is conducting non-qualifying activities, earning mainland UAE income above permitted thresholds, or failing to maintain adequate operational substance, it can all affect its qualifying status.

So, if a free zone business loses its QFZP status, it’s moved from 0% tax position to the standard 9% corporate tax rate, thus increasing tax exposure (in some cases, tax also applies retroactively.)

Another scope of risk is related party transactions. If transactions between connected entities are not conducted at arm’s length and properly documented, there’s a chance FTA may question the company’s qualifying position.

A Free Zone business may not lose its qualifying status because of one major error, but several smaller compliance gaps that pile up unnoticed over time.

If you underreport income, you create compliance risk. But if you overreport, you end up paying more tax than legally required.

The risk is great in both directions; underreporting taxable income can expose your business to FTA audits, back taxes, penalties, and increased scrutiny. On the other hand, overreporting can quietly drain cash flow through unnecessary tax payments that could’ve been avoided with proper structuring and review.

Taxable income is not always the same as accounting profit according to UAE law. Several adjustments may need to be made before arriving at the final taxable income figure.

Companies that tend to overlook related party transactions may need adjustment for transfer pricing based on arm’s length standards. Interest income from intercompany loans, gains from asset sales, and fringe benefits offered to employees can also affect taxable income calculations.

Regarding expenses, there are various cases where firms make improper deductions, including business entertainment expenses, penalties, and personal expenses incurred by company officials. Improper calculation of depreciation is another typical issue in accounting.

Managing corporate tax internally carries its own risk, especially if requirements are underestimated. Companies that manage tax filling in-house without specialized expertise risk getting an FTA notice, a potential audit, or learning later on that key obligations were missed.

Sometimes, the complexities of VAT and corporate tax filling may be left to the existing accountant. This move seems like it can reduce costs on outsourcing. This kind of reactive compliance can prove to be more expensive and time-consuming than intended.

The line between a bookkeeper, an accountant, and a corporate tax advisor is often blurred. It’s important to note that a bookkeeper may record transactions accurately, and an accountant may prepare financial statements, but a corporate tax consultant in Dubai interprets regulations, assesses tax exposure, reviews structuring risks, and ensures filings align with UAE corporate tax law.

By the time it becomes obvious to seek help, a small issue turns into a larger, more urgent, and more expensive mistake to fix. In such situations, teams often acknowledged that had they addressed it earlier, the problem wouldn’t have escalated.

There’s no room for discrepancies and misunderstandings in corporate tax. A single error becomes an expensive liability that can ultimately lead to penalties, corrective filings, and audit exposure. So, instead of treating compliance reactively, managing it consistently throughout the year can bring efficiency in the tax filling process.

That is why more UAE businesses are moving toward ongoing financial and tax support rather than relying on last-minute filing alone. With over 25 years of experience, The Total CFO has built a reputation as a leading tax advisory firm for businesses across the UAE.

We help companies stay aligned with ever-evolving FTA requirements through robust bookkeeping, VAT management, and corporate tax compliance, so you get a clear view into your financial position and conduct operations efficiently.Haven’t registered for corporate tax or are unsure about your current compliance status? Start with professional corporate tax registration guidance.

Some of the most common mistakes include treating corporate tax as a once-a-year task, assuming VAT compliance automatically covers corporate tax obligations, failing to maintain QFZP status in Free Zones, miscalculating taxable income, and delaying professional tax consultation.

No. VAT and corporate tax are separate tax regimes in the UAE. Each has its own registration requirements, filing deadlines, calculations, and compliance obligations. Being VAT compliant does not mean your business is automatically compliant with corporate tax regulations.

Yes. Free Zone businesses must continuously maintain their Qualifying Free Zone Person (QFZP) status. Conducting non-qualifying activities, exceeding mainland income thresholds, or failing substance requirements may result in losing the 0% tax benefit and becoming subject to the standard 9% corporate tax rate.

Proper bookkeeping helps businesses maintain accurate financial records, track deductible expenses, prepare compliant tax returns, and reduce the risk of penalties or FTA scrutiny. Poor record management can lead to errors, missed deductions, and filing complications.

Incorrect taxable income calculations can either expose a business to penalties and audits through underreporting or result in unnecessary tax payments through overreporting. Adjustments for related-party transactions, depreciation, entertainment expenses, and asset gains must be properly reviewed under UAE corporate tax law.

Corporate tax regulations can be complex and continuously evolving. Professional tax consultants help businesses understand compliance obligations, minimize tax risks, maintain proper documentation, and avoid costly penalties or corrective filings from the Federal Tax Authority (FTA).

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test