2026-06-19

Your financial statements have been audited. The report is signed. Everything appears in order.

So if the Federal Tax Authority (FTA) is to review your business tomorrow, you should be covered…right? Well, not necessarily.

One of the most common assumptions business owners and finance leaders often make is confusing an external audit with an FTA audit.

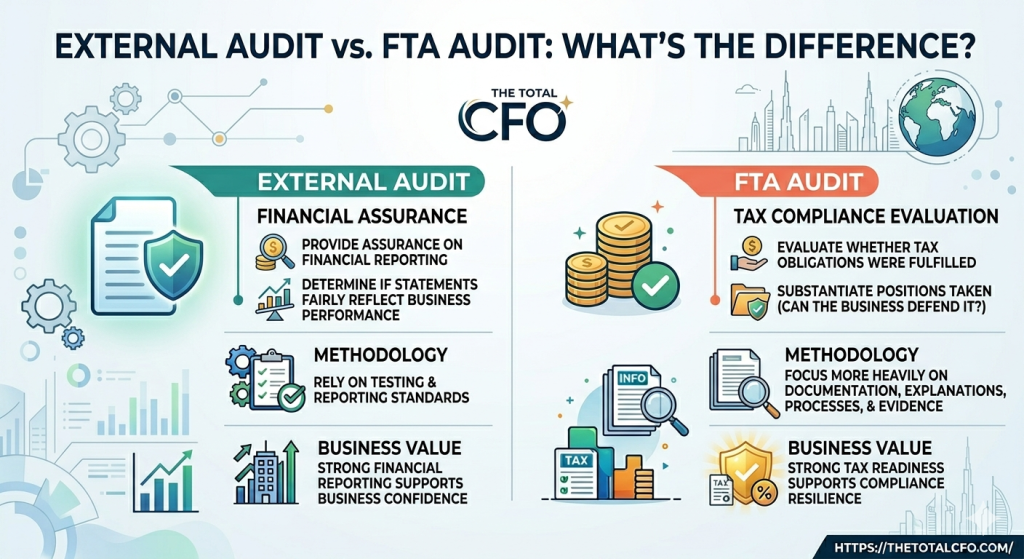

While the two may both involve reviewing financial information, their purposes are quite distinct. The former focuses on whether your financial statements fairly represent the financial position of the business, and an FTA audit is done to make sure your business complies with tax law.

Before you think they are the same and create unnecessary exposure, take some time to understand the consequences and applications of each method in this blog.

Now this can catch many businesses off guard. With an external audit, you can strengthen financial governance and demonstrate that financial statements have been prepared properly. However, it doesn’t guarantee full compliance with UAE tax obligations.

It’s because an external audit focuses on accuracy and presentation of your financial statements in accordance with accounting standards, while an FTA audit raises the question whether the business has complied with tax law and can back its tax filings.

Suppose your external auditor concludes that revenue was recorded duly in the financial statements. This doesn’t confirm whether the transaction received the correct tax treatment, the adjustments were properly documented, or whether filings align with regulatory requirements.

It’s important to note that tax authorities don’t just look at the final numbers reported — they demand transparency on the entire process, including records and evidence. Thus, a clean audit opinion is never a confirmation that your business is protected from future tax scrutiny.

Audited financial statements don’t reduce compliance risk automatically. In some situations, penalties often arise from areas that external audits were never intended to address.

The first problem that could lead to penalties would be a lack of documentation. Financial statements may seem accurate, yet when the business is asked for documentation proving transactions, records are often incomplete, difficult to retrieve, or spread across different systems.

Another challenge is undocumented tax positions. Teams may understand why decisions were made at the time, but if that reasoning was never formally recorded, it becomes difficult to explain later.

Differences between accounting treatment and tax treatment can also create issues. These differences are not necessarily incorrect, but businesses should be able to justify them and show how they were calculated.

Finally, fragmented processes and unclear ownership can lead to inconsistencies, especially when the process of recording relies on spreadsheets, manual workflows, or unclear reporting. At this point, businesses only end up discovering weaknesses once questions are raised.

FTAX readiness must be approached as an ongoing business discipline and not as a reactive process once an FTAX notice is received.

Begin by confirming that the numbers reported in the tax returns are able to be traced back to the accounting and other relevant documentation. Documentations for the tax positions, assumptions, and adjustments must also be clear and detailed enough for decision-making to be explained and understood in the long run.

It will help businesses determine if there are still inconsistencies between the accounting and tax process, keep documents which can easily be accessed, and determine weaknesses in the process even before becoming a problem.

Decreasing dependency on spreadsheets and manual processes might be helpful as well. The aim here is not for zero risks but being prepared for contingencies.

An external audit continues to be a critical component of financial governance and business credibility. It is not intended to provide false security concerning tax readiness.

There is a link between financial reporting assurance and tax compliance. Yet, they are different.

Businesses that get this are often able to react more confidently and avoid unnecessary disruptions, thus becoming better prepared from a compliance standpoint.

All in all, being audit ready is how you end the year, and being FTA ready is how you protect it.

And for being both, a team of qualified financial experts in the UAE can assist you. At The Total CFO, our experienced corporate tax consultants in Dubai conduct a holistic analysis of your financial performance and tax liabilities to help you stay FTA compliant with proper record keeping and accurate tax treatments.

No. An external audit verifies whether financial statements fairly represent a company’s financial position according to accounting standards. An FTA investigation focuses on tax compliance, supporting documentation, tax treatments, and the accuracy of tax filings.

An external audit assesses the accuracy and presentation of financial statements, while an FTA audit examines whether a business has complied with UAE tax laws, maintained proper records, and correctly reported its tax obligations.

Penalties often arise from issues such as missing documentation, undocumented tax positions, incorrect tax treatments, or inconsistencies between accounting records and tax filings. These areas may not be fully covered during an external audit.

Businesses should maintain tax invoices, contracts, accounting records, tax return workings, supporting calculations, correspondence related to tax decisions, and any documentation that supports the tax treatment of transactions.

Businesses can improve readiness by documenting tax positions, ensuring tax returns reconcile with accounting records, maintaining organized records, conducting periodic compliance reviews, and reducing reliance on manual processes and spreadsheets.

FTA readiness helps businesses respond confidently to tax authority reviews, reduce the risk of penalties, avoid operational disruptions, and demonstrate compliance with UAE tax regulations through accurate records and supporting evidence.

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test