2026-07-18

There is a lot going on in terms of financial compliance in the UAE right now and it shows no signs of slowing down, especially when you look ahead to what the future holds in 2026 and 2027.

What was once a relatively simple compliance environment now demands far greater financial transparency, accurate reporting, and stronger internal controls. This is evident in Corporate Tax and VAT compliance to Ultimate Beneficial Ownership (UBO), ESR, AML, and audit expectations.

The challenge for many companies is that it’s not just about filing returns on time. It’s about building systems, processes, and financial visibility that can withstand the regulatory oversight and support your business growth.

Several major shifts are happening all at once, making the next couple of years critical for businesses operating within the UAE.

The UAE is set to establish itself as a leading and trusted business and investment destination. And for that, it’s focused on strengthening its financial and regulatory ecosystem. Over the past few years, the introduction of Corporate Tax, expanding VAT enforcement, stricter AML obligations, and increased reporting requirements have drastically changed how businesses operate and manage compliance.

Additionally, the UAE is continuing to align with international best practices, focusing on proper accounting, documentation, beneficial ownership disclosures, and internal controls. There’s also heavy investment being made in digitizing tax administration and reporting, making it easier to detect any anomalies or compliance lapses.

While most businesses are subject to growing compliance requirements, the impact will be especially significant for large enterprises, multinational firms, free zones business entities, SMEs, and firms operating in regulated industries.

These organisations are likely to experience increased scrutiny around financial reporting, tax compliance, documentation, governance, and audit readiness as UAE regulations continue to tighten through 2026 and 2027.

Here are some significant requirements businesses must be aware of:

The future e-invoicing system in the UAE will necessitate companies to process their invoices digitally. For such processes to be successful, the company is supposed to hire an Accredited or Approved Service Provider that adheres to the technical requirements put forth by the UAE government.

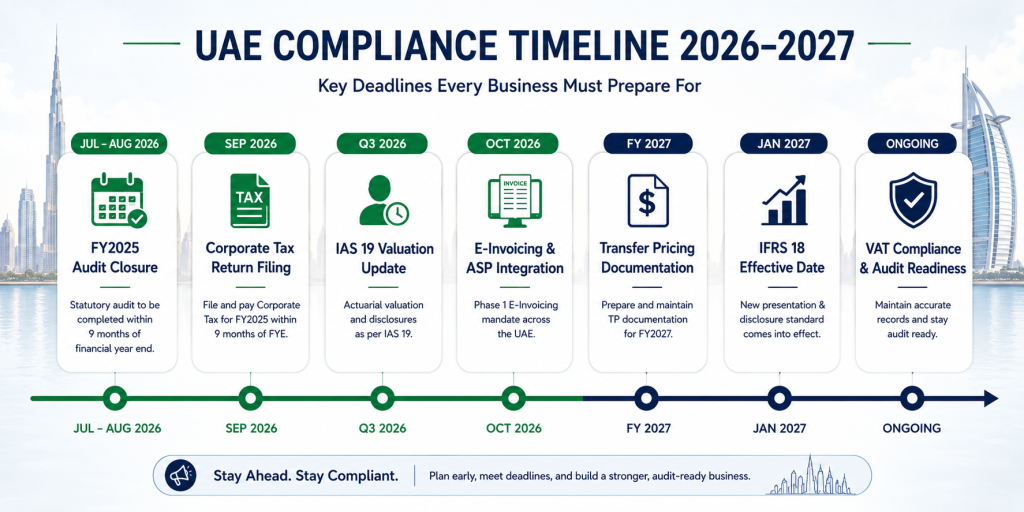

With effect from 30th October 2026, preparations for this must not be delayed. Businesses that still rely on outdated invoicing software might experience disruptions in processing their invoices.

A timely closure of the financial year 2025 will be crucial as government regulators, banks, and tax authorities focus more on financial accuracy.

Most companies experience delays in their audits owing to discrepancies in their reconciliation, lack of proper documentation, poor internal control procedures, or bad book-keeping. Adequate preparation can enable businesses to circumvent last minute problems that might affect financing, taxation, or regulatory filing requirements. Partnering with reliable bookkeeping services in Dubai can help businesses maintain accurate records and streamline audit readiness.

As Corporate Tax enforcement matures, it becomes necessary for the business to be well-prepared for filing obligations, disclosures, and supporting documentation requirements.

This involves maintaining accurate accounting records, properly categorizing expenses, supporting tax positions with documentation, and making sure that the disclosures are consistent with financial statements. Common filing issues include poor recordkeeping, incorrect tax adjustments, incomplete disclosures, and late submissions, all of which may increase audit exposure and penalty risk. With the guidance of experienced corporate tax consultants in Dubai, businesses can minimize compliance risks and streamline the filing process effectively.

Businesses with employee end-of-service benefit obligations may need actuarial valuations under IAS 19 to accurately reflect liabilities within their financial statements.

Deferred taxation is also gaining more relevance due to the new UAE Corporate Tax law. Such calculations will have a significant influence on accounting, profits, and overall correctness of the company’s activities.

Entities conducting business with related parties or connected persons must determine whether transfer pricing principles apply to their businesses.

Transfer pricing in UAE documentation normally consists of benchmarking reports, master files, and local files to establish that transactions between related parties take place on an arm’s length basis. Entities in the UAE without proper documentation may be subject to scrutiny and adjustments in the coming years.

The OECD framework regarding Pillar II establishes a system of global minimum tax rules which can be relevant to large multinational groups operating in the UAE.

Organizations falling within scope need to assess how top-up tax calculations, global effective tax rates, and reporting requirements could affect their organizational structure and tax exposure. Although the implementation of the measures is expected to affect only larger organizations, preparations are becoming more crucial for multinational enterprises.

IFRS 18 introduces significant changes to how businesses present and classify financial information within their financial statements.

Companies may need to restructure reporting formats, revise presentation methodologies, and prepare comparative restatements ahead of implementation deadlines.

With the increasing FTA audit activity, UAE tax enforcement is set to become more sophisticated and data-driven.

Businesses must maintain accurate VAT records, reconciliations, invoices, and supporting documentation to respond efficiently if audited. Poor recordkeeping, inconsistent filings, or unsupported VAT claims can lead to significant penalties, disputes, and operational disruption during reviews. Businesses should consider working with an experienced VAT consultant in Dubai to ensure compliance and reduce the risk of penalties during audits.

First, corporate tax enforcement is expected to become stricter. Early filings that were done as a basic registration exercise may lead a business to face deeper reviews around documentation, transfer pricing, expense treatment, and financial reporting accuracy. This is why many companies are increasingly relying on professional accounting services in Dubai to maintain proper financial records and ensure compliance readiness.

Second, there is expected to be an uptick in VAT compliance checks and audits. Any company that struggles with inaccurate bookkeeping, poor invoice management, or ineffective reconciliations is likely to run into problems during the FTA inspection process.

Third, expectations for international reporting have increased. As the UAE continues solidifying its reputation as a trustworthy location for international business, local firms have to meet increasing demands regarding transparency, money laundering prevention, reporting of beneficial ownership, and sound financial practices.

Before the compliance pressure starts growing, businesses must assess their current processes related to accounting, taxes, and reporting. This assessment will help detect any vulnerabilities regarding record-keeping, documentation, and financial controls.

In light of growing demands for well-organized and precise financial documents, it is important for companies to improve their financial documentation process. This includes internal control practices to ensure no errors in financial reports.

In anticipation of further digitalization of compliance in the UAE, business organizations must make sure that their accounting and ERP software is up-to-date.

The services of experts in compliance and taxation will be essential for businesses to stay up to date and avoid compliance and reporting mistakes.

With multiple deadlines approaching between 2026 and 2027, businesses should create structured compliance calendars to track filings, audits, disclosures, and reporting obligations across departments.

Ongoing training on the changes in UAE tax and compliance laws will help your company stay prepared and compliant with all rules.

In case of non-compliance, businesses can expect these consequences:

Failure to comply with tax and other obligations may attract fines, penalties, and interest charges for the UAE-based business entity. Even small discrepancies or omissions in financial reports may pose a serious risk.

Non-compliance with regulations may harm the business image among its customers, partners, banks, and other stakeholders. A company may be perceived as unreliable if its compliance records are poor.

Companies that have poor document management, inconsistent reporting, and other problems may face higher risks of detailed audits and reviews conducted by financial regulators.

Managing compliance risks on an ad hoc basis may result in operational challenges for companies, especially when it comes to audits or dealing with tax authorities.

Effective financial compliance management is critical to achieving certain goals, such as expanding the scope of operations, securing investment, getting financing, etc.

Companies which start to prepare ahead for the new era of regulations within the UAE environment will be much more equipped to handle the situation with confidence and stability. Early preparations can help companies minimize risks, errors, penalties, and even audits because the company is now operating efficiently by improving its financial management process.

Compliance also promotes higher levels of transparency when it comes to a firm’s financials, thereby helping the firm make sound strategic decisions as well as maintain accurate reports. The company also earns the trust and credibility of investors, bankers, and regulators in the process. Compliance requirements will only grow further during the years from 2026 to 2027.

The upcoming 2026-2027 compliance wave will lead to more strict Corporate Tax compliance, higher scrutiny of VAT, the need for e-invoicing, transfer pricing and stricter financial reporting throughout the UAE. The question is, are you prepared enough to handle these compliance challenges and mitigate possible risks?

With seasoned tax consultants by your side, you can turn these challenges into opportunities. The Total CFO helps businesses across the UAE strengthen compliance, and improve financial governance from day one. We bring a combined expertise of 100+ years and offer proactive support in tax and VAT compliance to audits, reporting, transfer pricing, and e-invoicing.

Ready to assess your compliance readiness before the pressure increases? Book a free tax consultation today.

UAE businesses should prepare for several major compliance developments, including Corporate Tax filings, VAT audit preparedness, e-invoicing implementation, transfer pricing documentation, IFRS 18 reporting changes, IAS 19 actuarial valuations, and increased AML and UBO reporting obligations.

The UAE’s e-invoicing framework is expected to move forward from October 2026. Businesses will need to adopt compliant digital invoicing systems and work with Accredited Service Providers (ASPs) to meet regulatory requirements.

Transfer pricing rules apply to businesses conducting transactions with related parties or connected persons. Companies may need benchmarking studies, master files, and local files to demonstrate that transactions are conducted at arm’s length and comply with UAE Corporate Tax regulations.

Businesses can prepare by maintaining accurate bookkeeping records, organizing invoices and supporting documents, performing regular reconciliations, and ensuring consistency between tax filings and financial statements. Strong internal controls and professional tax support also reduce audit risks.

Non-compliance can result in penalties, interest charges, increased audit scrutiny, reputational damage, operational disruptions, and challenges in securing financing or expanding the business. Poor financial reporting may also affect investor and banking relationships.

Professional tax consultants help businesses manage Corporate Tax, VAT compliance, transfer pricing, audit readiness, financial reporting, and e-invoicing implementation. They also assist in identifying compliance gaps, reducing risks, and ensuring businesses stay updated with evolving UAE regulations.

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

With over 25 years in Dubai and nearly 30 years as a Chartered and Management Accountant, Hemant has extensive experience across manufacturing, services and technology sectors. He has worked with major corporate groups including Al Tayer, Saif Al Ghurair, Dhabi, and Aditya Birla. Hemant specializes in profitability and cost management, debt restructuring, contract management, and regulatory compliance, having generated approximately USD 47.5 million in savings and profit growth. A confident public speaker and Distinguished Communicator, he lives by the quote: “You get what you reward for. If you want ants to come, you put sugar on the floor” (Charlie Munger), embodying his belief that “Profit has its own intelligence.”

Archana Mundhra is a qualified Chartered Accountant with over 15 years of experience in multinational corporations. Her proficiency lies in financial planning and business intelligence. Her deep financial understanding and profound analytical skills empower her to assist management in realizing their objectives effectively.

Rinkle Jain is a qualified Chartered Accountant and Fellow Member of the Institute of Chartered Accountant of India. A results-driven Chartered Accountant with a distinguished career marked by proficiency in management, financial planning, and catalyzing overall company development.Demonstrates a unique blend of financial acumen, strategic insight, and leadership prowess, contributing significantly to organizational success.

test